All Categories

Featured

Table of Contents

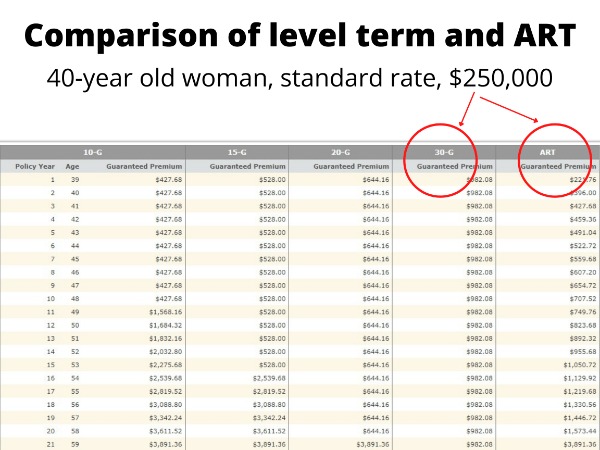

If you pick level term life insurance policy, you can allocate your costs since they'll remain the very same throughout your term. Plus, you'll understand precisely just how much of a death benefit your beneficiaries will certainly receive if you die, as this amount won't change either. The prices for degree term life insurance policy will certainly rely on a number of variables, like your age, health condition, and the insurance provider you choose.

As soon as you go with the application and medical test, the life insurance policy firm will certainly assess your application. Upon approval, you can pay your first premium and authorize any kind of relevant documents to guarantee you're covered.

You can select a 10, 20, or 30 year term and delight in the included peace of mind you deserve. Working with a representative can help you locate a plan that works ideal for your demands.

As you search for methods to protect your monetary future, you have actually likely stumbled upon a wide array of life insurance policy alternatives. term to 100 life insurance. Picking the best protection is a big choice. You want to locate something that will help sustain your loved ones or the reasons essential to you if something occurs to you

Many individuals lean towards term life insurance policy for its simplicity and cost-effectiveness. Term insurance contracts are for a reasonably short, specified amount of time however have choices you can customize to your requirements. Specific benefit choices can make your premiums alter in time. Level term insurance policy, nonetheless, is a kind of term life insurance policy that has regular payments and a changeless.

Dependable Term Life Insurance For Couples

Degree term life insurance policy is a part of It's called "level" because your premiums and the advantage to be paid to your enjoyed ones remain the same throughout the contract. You will not see any adjustments in cost or be left questioning its worth. Some contracts, such as every year sustainable term, may be structured with costs that enhance gradually as the insured ages.

They're figured out at the beginning and remain the same. Having regular payments can aid you far better strategy and budget since they'll never ever change. Dealt with death benefit. This is additionally set at the start, so you can understand exactly what survivor benefit amount your can anticipate when you pass away, as long as you're covered and updated on premiums.

This frequently in between 10 and 30 years. You consent to a set premium and survivor benefit for the period of the term. If you die while covered, your survivor benefit will be paid out to loved ones (as long as your costs depend on day). Your recipients will know beforehand how a lot they'll obtain, which can help for preparing objectives and bring them some monetary safety.

You may have the alternative to for another term or, most likely, restore it year to year. If your agreement has a guaranteed renewability clause, you might not need to have a brand-new medical exam to keep your insurance coverage going. Your premiums are likely to enhance due to the fact that they'll be based on your age at revival time.

With this choice, you can that will certainly last the rest of your life. In this case, again, you might not require to have any type of new clinical tests, yet costs likely will rise because of your age and brand-new protection. increasing term life insurance. Different firms provide numerous options for conversion, make sure to recognize your options before taking this step

Innovative Joint Term Life Insurance

Talking with a monetary consultant additionally might aid you identify the path that aligns best with your total strategy. Many term life insurance policy is level term throughout of the contract period, however not all. Some term insurance might come with a premium that enhances with time. With reducing term life insurance, your fatality benefit goes down with time (this kind is often gotten to particularly cover a long-term financial debt you're settling).

And if you're established for renewable term life, then your costs likely will increase each year. If you're checking out term life insurance policy and wish to guarantee uncomplicated and predictable financial security for your family members, level term might be something to think about. As with any type of insurance coverage, it may have some restrictions that don't satisfy your needs.

Value Level Term Life Insurance

Generally, term life insurance policy is much more inexpensive than long-term coverage, so it's a cost-effective way to secure financial security. At the end of your agreement's term, you have multiple choices to continue or relocate on from protection, frequently without needing a clinical examination.

Just like other type of term life insurance coverage, as soon as the contract ends, you'll likely pay higher premiums for insurance coverage due to the fact that it will recalculate at your existing age and health. Fixed protection. Level term supplies predictability. If your financial situation modifications, you may not have the essential coverage and could have to purchase additional insurance policy.

That doesn't indicate it's a fit for every person. As you're buying life insurance policy, below are a few key factors to think about: Budget. Among the advantages of degree term protection is you recognize the expense and the death benefit upfront, making it less complicated to without worrying regarding increases in time.

Age and health and wellness. Normally, with life insurance policy, the healthier and younger you are, the extra cost effective the insurance coverage. If you're young and healthy and balanced, it may be an appealing alternative to lock in reduced costs now. Financial obligation. Your dependents and economic responsibility contribute in establishing your insurance coverage. If you have a young family members, for example, degree term can help provide financial backing during important years without paying for coverage much longer than essential.

1 All riders undergo the conditions of the biker. All riders may not be readily available in all territories. Some states may vary the terms (what is level term life insurance). There might be a service charge linked with getting certain motorcyclists. Some cyclists might not be available in mix with various other cyclists and/or policy features.

2 A conversion credit score is not readily available for TermOne plans. 3 See Term Conversions area of the Term Collection 160 Item Overview for just how the term conversion credit rating is identified. A conversion credit scores is not available if premiums or charges for the brand-new policy will be forgoed under the terms of a rider providing disability waiver benefits.

Group Term Life Insurance Tax

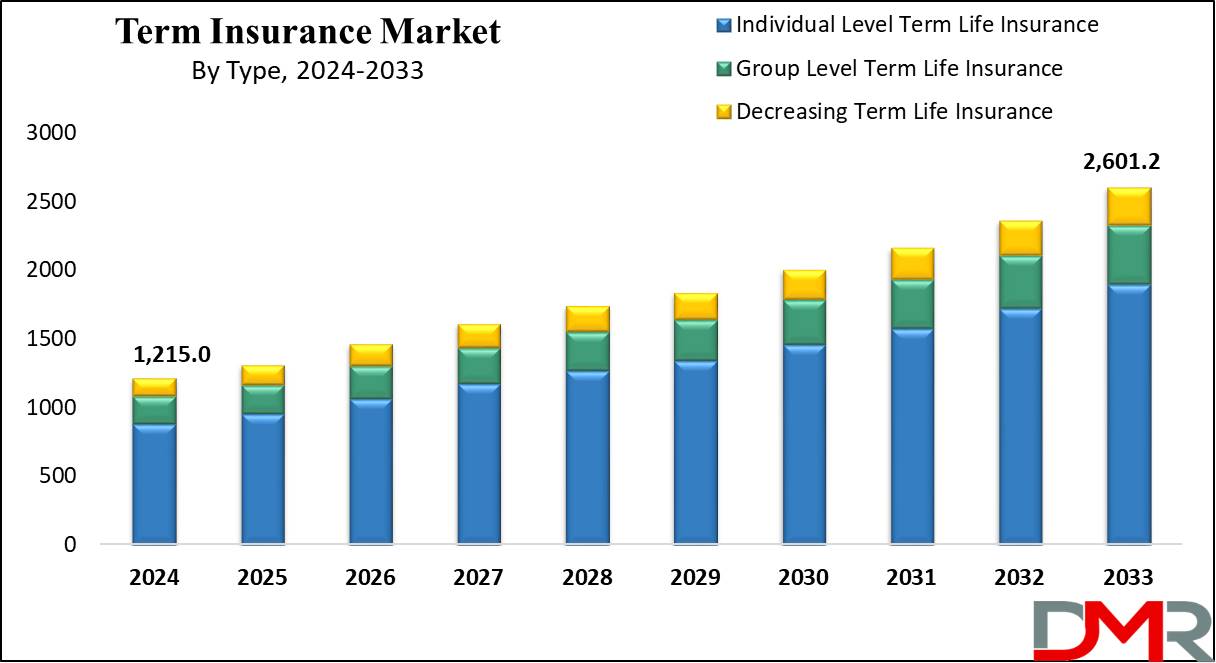

Term Collection items are released by Equitable Financial Life Insurance Policy Firm (Equitable Financial) (NY, NY) and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Coverage Firm of California, LLC in CA; Equitable Network Insurance Coverage Agency of Utah in UT; and Equitable Network of Puerto Rico, Inc. Term Life Insurance is a kind of life insurance plan that covers the insurance policy holder for a specific quantity of time, which is understood as the term. Terms normally range from 10 to 30 years and rise in 5-year increments, giving degree term insurance policy.

{kind=link}

Table of Contents

Latest Posts

Funeral Policy Without Waiting Period

Final Care

Final Expense Mailer

More

Latest Posts

Funeral Policy Without Waiting Period

Final Care

Final Expense Mailer