All Categories

Featured

Table of Contents

That generally makes them an extra affordable choice permanently insurance policy protection. Some term plans might not maintain the premium and survivor benefit the exact same with time. You do not wish to mistakenly believe you're purchasing degree term insurance coverage and after that have your death benefit modification in the future. Many individuals get life insurance protection to aid monetarily shield their liked ones in instance of their unforeseen fatality.

Or you might have the alternative to transform your existing term protection into a long-term plan that lasts the rest of your life. Different life insurance policy plans have possible benefits and drawbacks, so it's crucial to comprehend each before you choose to purchase a plan. There are several benefits of term life insurance coverage, making it a preferred choice for insurance coverage.

As long as you pay the premium, your beneficiaries will certainly get the fatality benefit if you pass away while covered. That stated, it is essential to note that many plans are contestable for 2 years which means protection can be retracted on fatality, should a misstatement be located in the application. Plans that are not contestable frequently have a rated survivor benefit.

Costs are normally less than entire life plans. With a degree term policy, you can choose your insurance coverage quantity and the policy size. You're not locked into a contract for the remainder of your life. Throughout your policy, you never have to fret about the costs or fatality benefit amounts changing.

And you can not squander your policy during its term, so you won't get any type of economic take advantage of your past coverage. Similar to other kinds of life insurance coverage, the expense of a degree term plan depends on your age, insurance coverage requirements, employment, way of living and wellness. Usually, you'll discover much more budget friendly coverage if you're more youthful, healthier and less dangerous to guarantee.

Guaranteed Joint Term Life Insurance

Considering that level term costs remain the very same for the duration of coverage, you'll know precisely how much you'll pay each time. That can be a large assistance when budgeting your costs. Degree term coverage additionally has some flexibility, allowing you to personalize your plan with added features. These frequently come in the form of motorcyclists.

You might have to fulfill specific problems and qualifications for your insurer to enact this biker. On top of that, there may be a waiting period of as much as six months before taking result. There likewise could be an age or time frame on the coverage. You can add a youngster rider to your life insurance policy plan so it likewise covers your kids.

The death advantage is commonly smaller, and coverage generally lasts up until your kid transforms 18 or 25. This rider may be a much more cost-efficient method to assist guarantee your kids are covered as cyclists can frequently cover several dependents at when. Once your youngster ages out of this insurance coverage, it may be possible to transform the motorcyclist right into a new plan.

When contrasting term versus permanent life insurance policy. level premium term life insurance policies, it's crucial to keep in mind there are a few various types. One of the most typical sort of irreversible life insurance policy is whole life insurance policy, however it has some key differences contrasted to level term protection. Below's a standard summary of what to think about when contrasting term vs.

Entire life insurance policy lasts forever, while term coverage lasts for a details period. The premiums for term life insurance policy are normally reduced than whole life protection. With both, the costs stay the exact same for the duration of the policy. Whole life insurance policy has a money worth component, where a portion of the costs may grow tax-deferred for future needs.

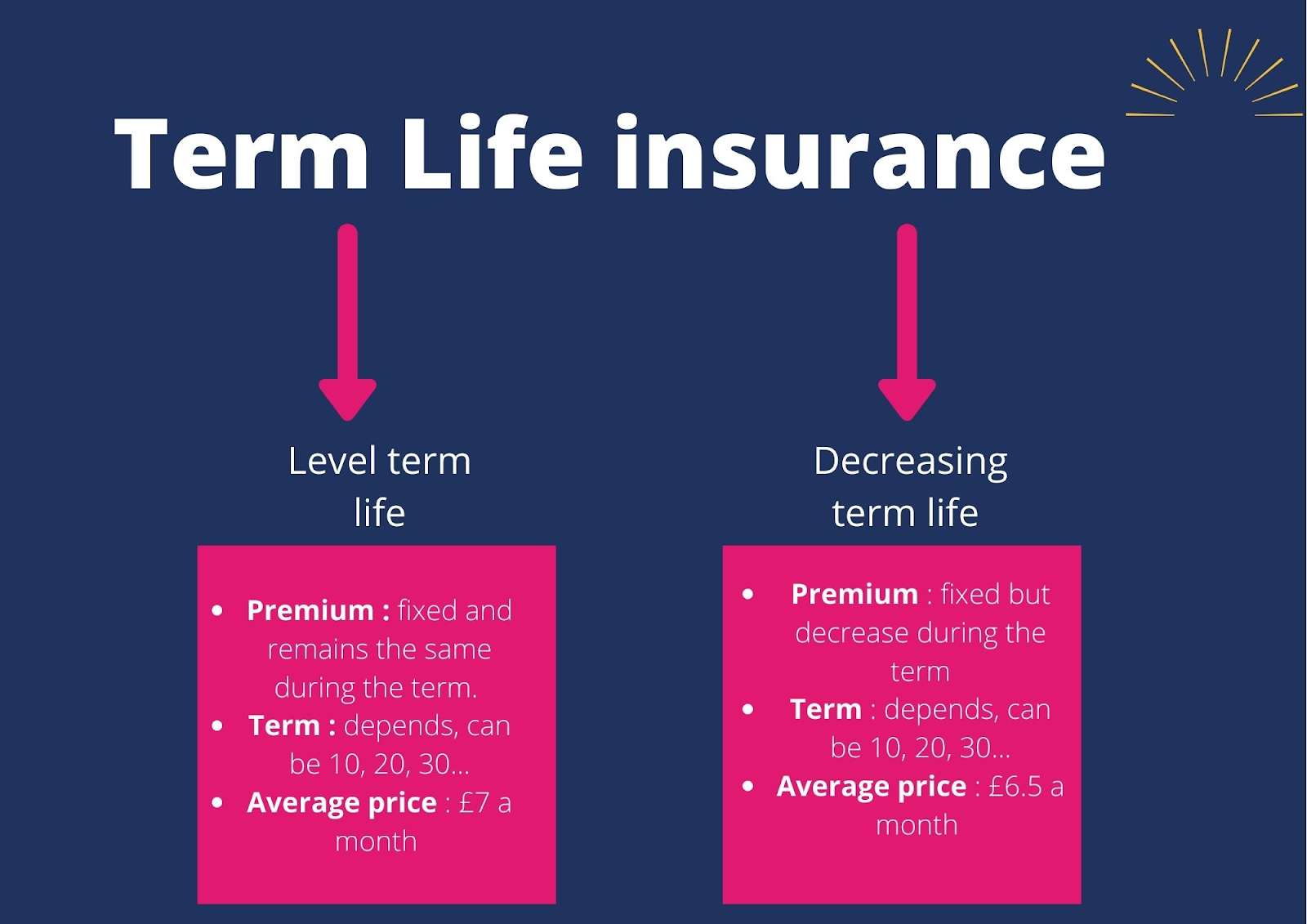

Among the highlights of level term protection is that your premiums and your survivor benefit do not alter. With decreasing term life insurance policy, your costs stay the same; however, the fatality advantage quantity obtains smaller sized gradually. You may have protection that begins with a fatality advantage of $10,000, which might cover a home mortgage, and then each year, the death advantage will reduce by a set quantity or percent.

Due to this, it's commonly an extra inexpensive sort of level term coverage. You may have life insurance coverage with your company, however it might not suffice life insurance coverage for your demands. The very first step when purchasing a plan is establishing exactly how much life insurance policy you require. Consider aspects such as: Age Household dimension and ages Employment standing Earnings Financial debt Way of living Expected final expenditures A life insurance policy calculator can aid identify just how much you need to start.

After making a decision on a plan, finish the application. If you're approved, sign the documentation and pay your initial premium.

Quality Short Term Life Insurance

Think about organizing time each year to assess your policy. You might want to update your beneficiary details if you have actually had any type of significant life changes, such as a marriage, birth or separation. Life insurance policy can sometimes feel difficult. However you do not have to go it alone. As you explore your choices, consider reviewing your requirements, wants and concerns with a monetary professional.

No, level term life insurance policy does not have cash money value. Some life insurance policy plans have a financial investment function that allows you to build cash money value over time. A part of your costs payments is alloted and can earn rate of interest gradually, which grows tax-deferred during the life of your protection.

Nonetheless, these policies are frequently significantly more costly than term coverage. If you get to completion of your policy and are still alive, the coverage ends. Nevertheless, you have some options if you still desire some life insurance policy protection. You can: If you're 65 and your insurance coverage has run out, for example, you might intend to purchase a new 10-year degree term life insurance coverage policy.

Flexible Level Term Life Insurance Definition

You may be able to convert your term coverage into an entire life policy that will certainly last for the rest of your life. Several sorts of level term policies are convertible. That implies, at the end of your insurance coverage, you can convert some or every one of your policy to entire life insurance coverage.

Degree term life insurance is a plan that lasts a collection term generally between 10 and three decades and comes with a level survivor benefit and degree costs that stay the very same for the entire time the plan is in effect. This implies you'll understand specifically just how much your settlements are and when you'll need to make them, allowing you to spending plan appropriately.

Degree term can be a terrific option if you're aiming to purchase life insurance policy coverage for the very first time. According to LIMRA's 2023 Insurance policy Measure Study, 30% of all grownups in the United state requirement life insurance and don't have any type of kind of policy. Level term life is foreseeable and cost effective, that makes it one of one of the most prominent types of life insurance.

{kind=link}

Table of Contents

Latest Posts

Funeral Policy Without Waiting Period

Final Care

Final Expense Mailer

More

Latest Posts

Funeral Policy Without Waiting Period

Final Care

Final Expense Mailer